GREED is Back and Upcoming PPI Report Likely Bearish

Early Innings of Trade Collapse and Jobs Market Weakening

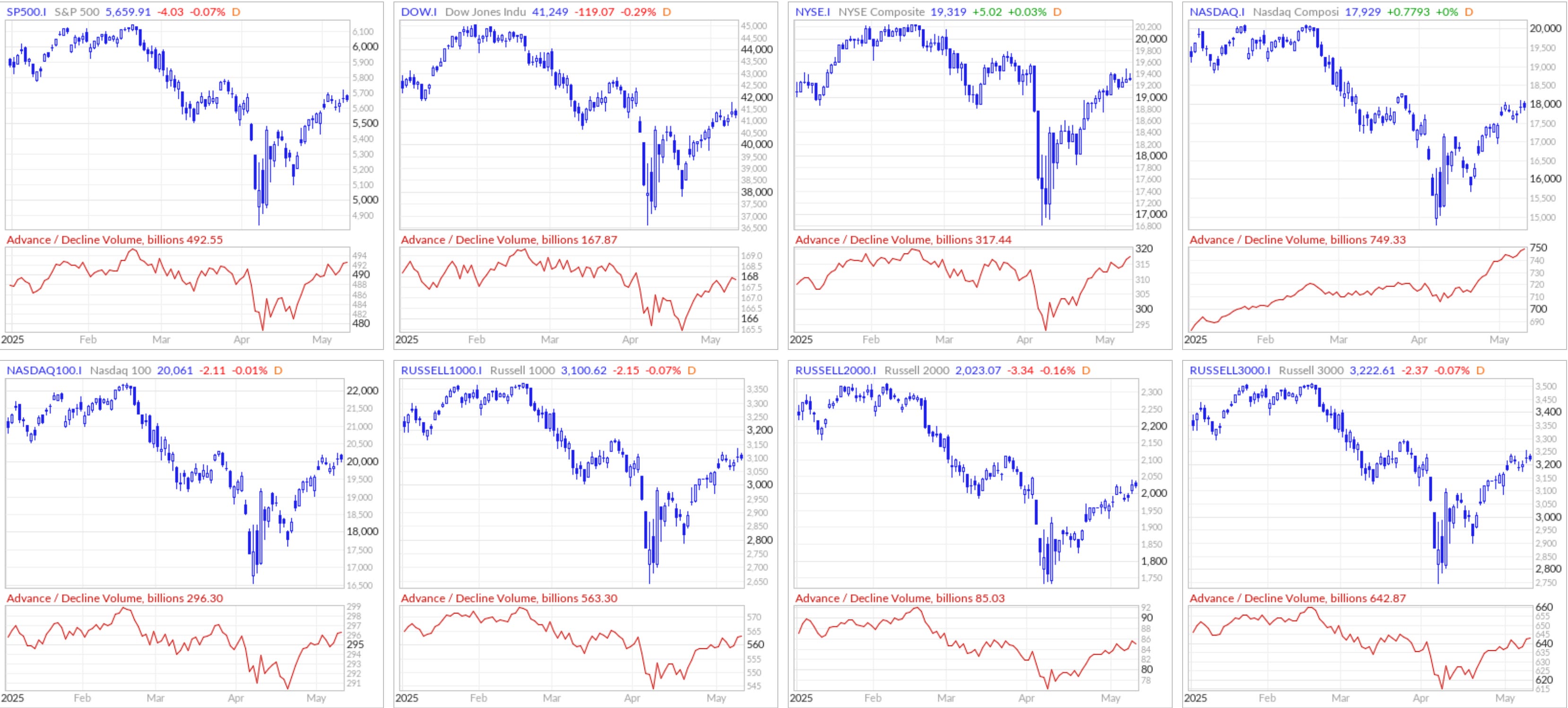

Recap

❓Below is my forecast regarding SPX 5700, so let’s see if I’m right this week

We’re back at Greed

New 52-Week Highs vs New 52-Week Lows

NYSE New 52-Week Highs: 50 vs New 52-Week Lows: 24

Nasdaq New 52-Week Highs: 93 vs New 52-Week Lows: 104 ← New 52-Week lows are now higher again, interesting shift and an early warning sign?

McClellan Oscillator seems to be losing bullishness

Advance/Decline Volume line

Nasdaq is extremely bullish

*This my personal blog and is not investment advice—I am not a financial advisor but a random person on the internet who does not have a license in finance or securities. This is my personal Substack which consists of opinions and/or general information. I may or may not have positions in any of the stocks mentioned. Don’t listen to anyone online without evaluating and understanding the risks involved and understand that you are responsible for making your own investment decisions.

We’re at the Early Innings of the Trade Collapse

Container volumes from China to the U.S. are collapsing and the data is starting to show up in real-time logistics activity, layoffs, and soon, consumer-facing shortages.

Supply chain expert, Craig Fuller, says are entering phase one of a multi-stage trade shock where he breaks down the phases below:

Phase 1: Logistics Pain, Job Losses Mounting

Container shipments from China have fallen off a cliff. Port volumes are dropping sharply, especially in Southern California, where over 500,000 workers depend on logistics activity. Truckers, warehouse staff, and distribution centers are already seeing fewer loads and route cancellations.

We’re still early in the cycle, but companies like UPS and Penske have already announced layoffs, and more are expected. With containerized imports accounting for ~20% of U.S. trucking volume, and trucking employment being tightly tied to demand, this collapse could mean 400,000–450,000 logistics jobs lost in the coming weeks.

Phase 2: Inventory Shortages for Consumers

As we head into summer, the downstream effect of this trade breakdown will start to hit store shelves. In June, you might notice odd gaps—missing sizes, colors, or SKUs. But the real consumer impact will be felt during Back-to-School season in August, when goods that were supposed to be shipped in April and May simply won’t be there.

Retailers have pulled orders from Chinese suppliers, leaving goods stranded in warehouses and factories across China. Inventory isn’t “just late”—in many cases, it was never shipped at all.

Phase 3: The Holiday Risk Window

If there’s no trade resolution by July, the situation gets much worse. U.S. companies aren’t placing new orders with Chinese manufacturers because they can’t absorb 145% tariffs. But without those new orders, holiday inventory won't arrive in time.

The supply chain lead time is about 3–4 months from contract to shelf. So if a deal isn’t struck by mid-summer, expect major product stockouts come November–December. Holiday sales season could be severely disrupted—especially for retailers dependent on imported electronics, apparel, and seasonal goods.

Trump Admin’s window to fix this is now. Otherwise, we’re headed for a consumer-facing squeeze.

Forecast

Powell's May 7th Remarks are indeed a net negative

Keep reading with a 7-day free trial

Subscribe to Best of Twitter/Threads, Analysis & Forecasts to keep reading this post and get 7 days of free access to the full post archives.